A major discussion in the tax world concerns the timing of the introduction of Pillar One and Pillar Two of the second phase of the Organisation for Economic Co-operation and Development (OECD) Base Erosion and Profit Shifting program (BEPS 2.0).

Pillar One

What is Pillar One?

Pillar One involves the reallocation to market jurisdictions of 25% of profit above 10% of very large multinationals with revenue exceeding 20 billion euros ($20.8 billion). There are exclusions for extractives and regulated financial services. It also involves changing existing tax treaties, which is proposed to be achieved through a multilateral Instrument of many countries signing up to the new rules through a streamlined mechanism.

Status Report

The timetable for the introduction of Pillar One in the agreements made by the Inclusive Framework of more than 130 countries on July 1 and October 8, 2021 proposed that the changes would take place from 2023.

Given the complexity of Pillar One, this was always going to be an ambitious timetable.

At Davos, the Secretary-General of the OECD, Mathias Cormann, indicated that the implementation of Pillar One would be delayed until 2024.

Questions have been raised as to the nature and prospects of the Pillar One rules passing the US Congress. Recently, US Treasury Secretary Janet Yellen indicated that the ratification process clearly requires the approval of Congress, but the form this needs to take is yet to be determined.

An essential feature of the agreement in relation to Pillar One is that countries agree to withdraw, or not to introduce, digital services taxes. This is the Damocles Sword. If agreement is not reached, then the world is likely to see the proliferation of these taxes, and potentially counter-measures on tariffs.

The OECD has estimated that this world—of no Pillar One, and with digital services taxes—could result in a significant reduction of global GDP. This is an important incentive to get Pillar One done.

India impact

India has agreed to withdraw the much controversial Google tax (a.k.a Equalisation levy) as part of its commitment to Pillar One initiatives. With the delay in implementation of Pillar One worldwide, the withdrawal will not be happening any time soon.

We can fully expect the controversies surrounding Equalisation levy to continue to grow for the time being.

Pillar Two

What is Pillar Two?

Pillar Two involves the introduction of a global minimum tax for multinationals with revenue greater than 750 million euros. The proposed rules seek to ensure that multinationals pay a minimum of 15% tax determined on a jurisdiction-by-jurisdiction basis by charging “top-up tax” if the Effective Tax Rate falls below 15%.

There are two important elements to note. The first is that the more than 130 countries that signed up to Pillar Two in the agreements of July 1 and October 8, 2021, did not agree to introduce the rules in their own jurisdiction (although many will) but not to introduce inconsistent rules.

Thus, Pillar Two does not rely on all countries agreeing to a minimum tax, but simply a sufficient number of countries agreeing to do so.

This raises the second important element. The top-up tax to ensure that a 15% rate is achieved on a jurisdictional basis can be levied at three levels. The first level is where a jurisdiction in which a multinational’s Constituent Entities are located introduces a domestic minimum top-up tax of 15%. Technically this is referred to as a Qualifying Domestic Minimum Top-up Tax, or QDMTT. This concept was introduced only in December 2021 and after the earlier Inclusive Framework agreements.

Jurisdictions will have a significant incentive to introduce a QDMTT because in the absence of such a tax, profits of multinationals from that jurisdiction could be taxed elsewhere under the other two levels.

The second level is the Income Inclusion Rule, or IIR. This rule is akin to a controlled foreign corporation rule and provides for top-up tax up the chain where a parent, including the ultimate parent or an intermediate parent, is located in a jurisdiction that has implemented the rule.

The third level is UTPR. This started off as an Undertaxed Payments Rule, but as it evolved such that the concept applies beyond payments, what used to be an acronym has become its actual name. It is the back-up policeman rule and can apply where a Constituent Entity of a multinational is located in a jurisdiction with such a rule, and there is unpaid top-up tax at the other two levels.

Status Report

On Pillar Two the agreements of July 1 and October 8, 2021 provided for the introduction of the IIR rule in 2023 and the UTPR rule in 2024.

However, discussions in the EU focused on converting the Inclusive Framework proposals into an EU directive reflected that this timing was too tight. At an Economic and Financial Affairs Council (Ecofin) meeting of April 5, 2022 it was agreed by 27 EU countries, except Poland, to implement the IIR from 2024 and not 2023, and the UTPR from 2025 and not 2024.

There were further potential deferrals for EU countries with 12 or fewer in-scope multinationals—basically multinationals with revenue more than 750 million euros—whose ultimate parent entity was located in that jurisdiction.

To date, Poland has taken the position that it will not sign up for Pillar Two unless Pillar One is fully agreed. Advice from the EU has suggested that such a linkage would be contrary to EU rules.

Going Forward—How Will Countries Proceed?

While the EU is broadly on a path of deferral for 12 months, it does not mean that other countries will follow suit. The position of the UK is not clear and the UK may well introduce an IIR in 2023 and the UTPR in 2024.

While many UK businesses would prefer to see a deferral to 2024 and 2025 in line with the EU path, there is a Brexit narrative that the UK can do things faster outside the EU, and potentially a revenue-raising incentive to go in 2023 for the IIR rule.

There are other countries, such as Indonesia and Australia, and potentially Japan, that suggest that they will introduce an IIR rule with a 2023 commencement date.

These countries may benefit from a first mover advantage, particularly if they have a UTPR rule in place in 2024 while others only introduce such a rule from 2025.

There is no reason why a country could not introduce an IIR and a UTPR in 2024. That is, the earliest a UTPR rule could be introduced is 2024, but it does not need to be introduced 12 months after the IIR rule.

The US position is different. They have rules in place currently, referred to as Global Intangible Low-Taxed Income (GILTI) rules, which require certain changes to ensure that they conform with the Pillar Two rules. In particular, GILTI is based on global blending rather than jurisdictional blending. If the EU and other countries have agreed to introduce global minimum tax rules, then this will assist in arguments for the US Congress to change their GILTI rules.

What do businesses need to know?

For businesses, the potential complexity of different countries introducing QDMTT, IIR, and UTPR rules at different times is considerable. Such complexity feeds into accounting issues on recognition of top-up tax generally once rules are substantively enacted. This is further complicated where laws are passed with retrospective effect; for example, a law passed on October 1, 2023 with effect from January 1, 2023.

Additional complexity arises where countries have straddle years, such as India, UK, Japan, which are likely to commence Pillar Two rules from April 1.

As far as India is concerned, the most significant impact would be on delay of withdrawal of Equalisation levy due to delay in implementing Pillar One.

We can expect volatile and dynamic times ahead in the fight against BEPS!

—–

We would love to hear from you.

For any clarifications or queries, please reach out to us at contact@vprpca.com

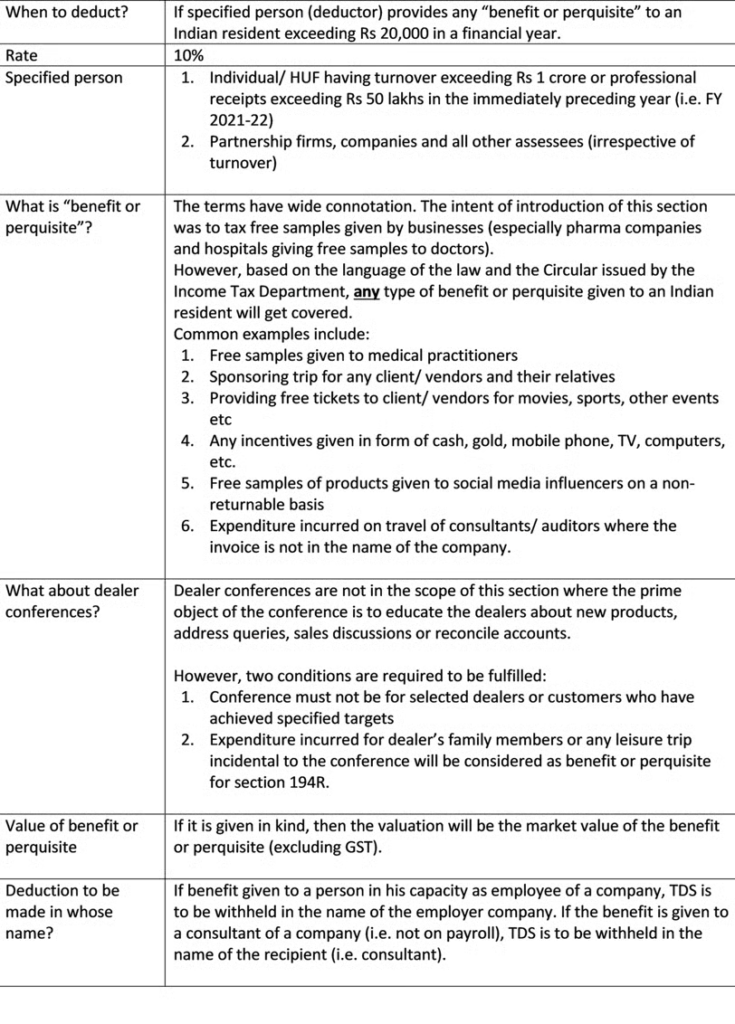

Budget 2022 has introduced a new section for tax deduction at source (TDS) – section 194R of the Income-tax Act, 1961.

This section is applicable with effect from 1 July 2022.

To further clarify the scope of the section, the Circular 12 of 2022 was issued by the Central Board of Direct Taxes. Guidelines in QnA format have been released in this Circular. However, it is important to note that as per law, a Circular is not binding on the taxpayers and is only binding on the Income tax department officials.

With that said, let us discuss what the section says:

Section 194R states that TDS is to be withheld at 10% if specified person (deductor) provides any “benefit or perquisite” to an Indian resident exceeding Rs 20,000 in a financial year.

The limit of Rs 20,000 is to be calculated for each recipient in a financial year.

Specified persons mean:

1. Individual/ HUF having turnover exceeding Rs 1 crore or professional receipts exceeding Rs 50 lakhs in the immediately preceding year (i.e. FY 2021-22)

2. Partnership firms, companies and all other assessees (irrespective of turnover)

What is “benefit or perquisite”?

The terms have wide connotation. The intent of introduction of this section was to tax free samples given by businesses (especially pharma companies and hospitals giving free samples to doctors).

However, based on the language of the law and the Circular issued by the Income Tax Department, any type of benefit or perquisite given to an Indian resident will get covered.

Common examples include:

1. Free samples given to medical practitioners

2. Sponsoring trip for any client/ vendors and their relatives

3. Providing free tickets to client/ vendors for movies, sports, other events etc

4. Any incentives given in form of cash, gold, mobile phone, TV, computers, etc.

5. Free samples of products given to social media influencers on a non-returnable basis

6. Expenditure incurred on travel of consultants/ auditors where the invoice is not in the name of the company.

Dealer conferences are not in the scope of this section where the prime object of the conference is to educate the dealers about new products, address queries, sales discussions or reconcile accounts. However, two conditions are required to be fulfilled:

1. Conference must not be for selected dealers or customers who have achieved specified targets

2. Expenditure incurred for dealer’s family members or any leisure trip incidental to the conference will be considered as benefit or perquisite for section 194R.

If it is given in kind, then the valuation will be the market value of the benefit or perquisite (excluding GST).

If benefit given to a person in his capacity as employee of a company, TDS is to be withheld in the name of the employer company. If the benefit is given to a consultant of a company (i.e. not on payroll), TDS is to be withheld in the name of the recipient (i.e. consultant).

Conclusion

To conclude, the new provisions are going to come into force from 1 July 2022. Every benefit given to a third party should be monitored and extensive documentation is to be maintained for the same.

Should you require any further clarifications or have any queries, please do reach out to us at contact@vprpca.com

Sections 80G(5) and section 35(1A) of the Income-tax Act, 1961 (hereinafter referred to as the Act) requires furnishing of statement of donation received and the issue of donation certificates to the donors for claiming deduction from the gross total income.

This notification has framed the rules for furnishing such statements and certificates of donation to donors. For this purpose, Rule 18AB was inserted vide Finance Act, 2021.

Notified form

These statements in Form 10BD are required to be e-filed by a registered Charitable Trust with Income Tax before 31st May 2022 giving the following information about the donations received by it whether general or corpus:

Name of the donor

PAN/Aadhar/Voting Card/Election ID of the donor

Amount of Donation in Rupees

Type of donation

All donations need to be reported.

There is no threshold available.

In case of no such donations received by the trust, Income Tax Portal has not allowed to file a NIL Form 10BD.

The trust is required to upload a CSV file on its Income Tax login page. There the system will take 24 hours to accept/reject this form and Form 10BE (Certificate of Donations) can be downloaded. These certificates must be downloaded before 31st May 2022.

Verification

Form 10BD can be signed by the authorized signatory/trustee by using Digital Signature Certificate or electronic verification code.

Late Fees

Any delay in e filing Form 10BD attracts late filing fees of Rs. 200 per day (Section 234G). Section 271K attracts a penalty of Rs. 10,000 to Rs. 1,00,000 for failure to file a statement of donation in Form 10BD.

In case of any clarification or information, please feel free to write to us at contact@vprpca.com

Every citizen of India is liable to pay tax if their income comes under the Income Tax bracket. The government depends mainly on its tax collection to finance its spending throughout the year. This funding is utilized in the development of nation, reforming infrastructure, and the betterment of society, which helps in shaping the economy of the country. There is a tax structure in India that is followed and as per the tax slabs; individuals are required to pay their taxes.

Let us understand about advance tax and how advance tax is calculated in India.

What is Advance Tax?

Advance tax is the amount of income tax that should be paid much in advance instead of lump-sum payment at the year-end in instalments as per the due dates given by income tax department. Advance tax is also known as ‘pay as you earn’ tax and is supposed to be paid in the same year the income is received.

Who Needs to Pay Advance Tax?

As per section 208 of Income-tax Act, 1961, a taxpayer needs to pay advance tax if their tax liability is 10,000 or more in a financial year.

Advance tax is for those who earn money from sources other than salary. It is applicable for self-employed individuals, professionals, and business men if their income exceeds a certain limit This includes money that comes from shares, interest earned on fixed deposits, rent or income received from house tenants. Senior citizens who are more than 60 years of age are exempt to advance tax.

How to Calculate Advance Tax?

Listed below are the 4 steps that will help you calculate advance tax:

1. Make an estimate of the total income earned by you.

2. Subtract all expenses from your income, including medical insurance premiums, phone costs, travel expenses, etc.

3. Now, add other income that you received apart from your salary. This includes interest from FDs, house rent, lottery earnings, etc.

4. If the amount of tax calculated is more than 10,000, then you are liable to pay advance tax.

How to Pay Advance Tax?

Just like regular tax payment, advance tax payment is also done using challan. There are many banks that allows you to pay advance tax through challans. You can also pay advance tax online from the comfort of your home. Here’s a step-by-step guide that will help you pay advance tax online without any hassles –

1. To pay advance tax online, you need to click on the government’s official website – http://www.tin-nsdl.com

2. Choose the correct challan that is ITNS 280, ITNS 281, ITNS 282 or ITNS 284 as relevant to pay your advance tax.

3. Fill in your PAN card details along with other important information such as your address, phone number, e-mail address, bank name, etc.

4. Once you have entered all the details, you will be redirected to the net-banking page of the website.

5. Now, you will receive all the information regarding your payment. Enter all payment details and pay your advance tax online successfully.

What are the Benefits of Advance Tax?

Here’s a list of benefits you get when you pay tax in advance –

1. It reduces the burden of paying tax at the last moment.

2. It helps in mitigating stress that a taxpayer may undergo while making tax payment at the end of fiscal year.

3. It saves people from failing to make their tax payments.

4. It helps in raising government funds as the government receives interest on the tax collected.

What are Due Dates for Payment of Advance Tax?

Here’s a schedule of advance tax payment for individual taxpayers –

15 June – 15% of advance tax liability

15 September – 45% of advance tax liability

15 December – 75% of advance tax liability

15 March – 100% of advance tax liability

1. What if I pay advance tax* less or more than required for a financial year?

The IT Act has provided four dates and the percentage of advance tax to be paid on each of these dates. If by chance you have paid the excess advance tax you would receive a refund subject to section 237 of the Income Tax Act with 6% interest per annum on the excess amount subject to Section 244A of the Act if the excess is more than 10% of the tax liability.

If on March 15, you find that you have a shortfall of advance tax to be paid you can still pay the advance tax before 31st March and the same would be treated as advance tax.

2. What is the penalty for missing the dates of payment of Advance Tax?

If you miss the dates for payment of advance tax you will be levied interest under section 234B and 234C of the Income tax Act.

3. Can I claim deduction under 80C while estimating income for determining my advance tax?

Yes, you can claim deduction under Section 80C while estimating income for determining your advance tax.

4. Is an NRI liable for payment of advance tax?

Yes, an NRI is liable for payment of advance tax on the income earned in India as per provisions of the Income tax Act in force for the relevant assessment year.

In case of any confusion or queries, please seek professional guidance.

India is the world’s fastest-growing economy and yet there is no mention of the Indian debt market on global indices. Most major economies are listed since a long time.

“India has made significant strides in macroeconomic stability, and its government is more motivated than ever to encourage corporate-investment-driven growth,” says Chief India Economist Upasana Chachra.

“We think India will be included in two of the three major global bond indices in early 2022.”

Beyond the direct benefits of index inclusion—it could trigger $170 billion in bond flows over the next decade, lifting Indian bond prices while lowering borrowing costs—this milestone could have profound implications for the country’s currency, corporate bonds and equities.

A few implications of global-bond-index inclusion for India, and why it could signal the emergence of a new India.

1. Immediate Boost for Government Bonds

Major indices don’t simply track their respective markets—they influence them. When an index adds new constituents, portfolios pegged to those benchmarks must adjust their allocations accordingly. “India’s inclusion would trigger significant index-related inflows, followed by an allocation from active global bond investors,” says Min Dai, Head of Asia Macro Strategy.

2. Shrinking Deficit, Stronger Rupee

Index inclusion, while significant on its own, would also signal policymakers’ desire to support higher economic growth through investment. “This will push India’s balance of payments into a structural surplus zone and indirectly create an environment for lower-cost capital and, ultimately, be positive for growth,” says Chachra, adding that India’s consolidated deficit could shrink to 5% of its GDP by 2029, down from 14.4% for the 2021 fiscal year.

India’s currency would also feel the impact. The shrinking deficit could bolster the value of the Indian rupee by 2% a year against a basket of other major currencies, in exchange rate terms. While India’s long-term 4% annual inflation would imply a 2% depreciation in the value of the rupee in nominal terms, at around a 6% yield, Indian government bonds could offer investors medium-term returns of around 4% in dollar terms, “which is quite attractive for foreign investors,” says Dai.

3. Capital needs of Corporates

Inclusion in global bond indices could also help Indian corporations with their capital needs. When foreign capital flows into government bond markets, it lowers overall borrowing costs, improves debt sustainability and also drives demand for other—read corporate—fixed-income securities. That’s potentially good news for India’s domestic corporate bond market, which foreign investors have largely overlooked.

Foreign investors would gain access to a significantly larger pool of Indian corporate issuers.

4. Equities Buoyed by Better Growth

The opening of India’s sovereign bond market may also bode well for equities, which stand to benefit from lower borrowing costs and a healthier macroeconomic backdrop. Among these, large private banks could be the most obvious winners. Still, nonbank financials— such as those focused on mortgages, credit cards, insurance and asset management—could enjoy the spillover effects of a more robust bond market in India.

Sources:

1. Morgan Stanley research report

2. India’s global indices report

3. RBI Press Release dated 8 October 2021

We would love to hear from you! Please get in touch at contact@vprpca.com

The concept of “beneficial ownership” (BO) plays a crucial role in determining whether a recipient of income qualifies for certain benefits under the Double Taxation Avoidance Agreement (‘DTAA’).

It is quite significant from international taxation perspective as a significant number of tax treaties adopt the condition of BO for granting concessional treatment to a resident of another country; in particular, when it comes to articles dealing with dividend, interest, royalties.

BO under tax treaties is a specific anti-abuse rule incorporated to target specific instances of tax treaty shopping involving the use of agents/ nominees/ conduits i.e. entities which act as mere administrators or fiduciaries of income and have no substance of their own.

From Indian perspective, the concept of BO has gained even more relevance with the abolishment of dividend distribution tax on companies whereby the dividend is now taxable in the hands of the investors with effect from 1 April 2020. The tax rate for a non-resident prescribed under section 115A of the Income-tax Act, 1961 (‘Act’) is 20% (plus applicable surcharge and health and education cess) while many India’s tax treaties typically provide a tax rate of 5-15% subject to BO and certain other shareholding related conditions. Thus, foreign investors exploring to avail benefit under the tax treaty would be required to fulfil the BO criteria.

To understand the methods for evaluating BO, it is imperative to first discuss the evolution of the concept in international tax arena.

Evolution of the concept of BO in tax treaties

The concept of BO was first envisaged in the US-Canada tax treaty of 1942 and has evolved over time.

The expression ‘beneficial owner’ has not been defined under the tax treaties or the Act and must therefore be interpreted based on general commercial understanding, tax commentaries and judicial precedents in this regard.

The Model Commentaries (MC) to the tax treaties and leading international tax lawyers have commented that the term has to be given a purposive interpretation (viz. prevention of tax avoidance) and persons not entitled to treaty protection are to be prevented from obtaining benefits there under by interposing entities between the ultimate beneficiary and the payer.

Further, in evaluating the concept of BO, one has to take cognizance of the ‘substance’ of the transaction and not its ‘form’ duly considering all relevant facts and circumstances. In other words, the meaning of the term “BO”, should be understood in a commercial or general parlance.

Definitions of beneficial owner

With regards to the term ‘beneficial owner’, as per Black’s Law Dictionary[1], the said term is defined as “one recognized in equity as the owner of something because use and title belongs to that person, even though legal title belongs to someone else.”

Law Lexicon defines ‘beneficial owner’ as “one who, though not having apparent legal

title, is in equity entitled to enjoy the advantage of ownership.”

As per Prof Klaus Vogel, among other factors, the issue of control is the most important factor in deciding the BO. Beneficial owner is the person who is free to decide:

Whether or not the capital or other assets should be used or made available for use by others; or

On how the yield there from should be used; or

Both

Further, Klaus Vogel in his commentary[2] also states that “….even a one hundred per cent interest in a subsidiary does not preclude the latter’s ‘beneficial ownership’ in the assets held by it. There would have to be other indications of the fact that the subsidiary’s management is not in a position to make decisions differing from the will of the controlling shareholders. If it were so, the subsidiary’s power would be no more than formal and the subsidiary would, therefore, not qualify as a “beneficial owner” within the meaning of Arts. 10 to 12.”

Reference from treaty commentaries

The OECD MC[3], in relation to the ‘BO’ was substantially amended in 2014. The key highlights of the commentary in relation to BO are as under:

The meaning of “beneficial owner” should be interpreted as not to refer to any technical meaning that it could have had under the domestic law of a specific country, but it must be understood in light of context and purpose of the tax treaty.

In addition to agent and nominees, conduit companies do not satisfy the status of BO.

It is considered that a direct recipient of income may not qualify as a “beneficial owner”, if from the very inception of his status, that recipient’s right to use and enjoy the income is constrained by a contractual or legal obligation to pass on the payment received to another person.

Reference has been made to the “related” and “unrelated” obligations. In case where the recipient has specific obligation to pass on the income received, such factor is relevant to the BO test.

The obligation may be inferred from legal documents or facts and circumstances of the case.

The concept of BO and other forms of anti-avoidance principles are applicable simultaneously since BO addresses specific forms of tax avoidance.

Reference from domestic and international Judiciary

Key Indian judicial precedents/ circulars etc. in the context of BO are set out below:

Circular No. 789 dated 13 April 2000 issued by the Central Board of Direct Taxes (CBDT) in the context of the Treaty provides that a Tax Residency Certificate (TRC) issued by the tax authorities of a country would be regarded as conclusive evidence regarding residential status and BO of the income earned by Mauritian entities. The validity of the above Circular has been confirmed by the Supreme Court in its decision in the case of Union of India v Azadi Bachao Andolan[4].

In Bharti Airtel Limited[5], the issue before the Income Tax Appellate Tribunal (ITAT) was whether benefit of Article 11 of the India-Sweden tax treaty would be available when interest was paid to an ‘arranger’ of loan (ABN Amro Bank, Sweden) instead of the actual lender. The ITAT held that the provisions of Article 11 shall not be applicable since the arranger is a mere conduit for onward payment to the actual lenders. Even though the arranger produced a TRC to establish their residency in Sweden, the interest received by the arranger was not in its own right but merely as a facilitator and thus the arranger is not the beneficial owner of the interest income.

In HSBC Bank (Mauritius) Ltd.[6], in context of BO of interest income, the ITAT adjudicated the following:

“Considering the above, we infer that the ‘beneficial owner’ can be the one with the full right and the privilege to benefit directly from the interest income earned by the FII-Bank (Indo-food International Finance Ltd vs. J.P. Morgan Chase Bank NA London Branch [2006] EWCA case 158). The income must be attributable to the assessee for tax purposes and the same should not be aimed at transmitting to the third parties under any contractual agreement / understanding. The bank should not act as a conduit for any person, who in fact receives the benefits of the interest income concerned. The recipient of the interest income should be deemed as the ‘beneficial owner’ unless there is any evidence to suggest that the said interest income is for the benefit of third persons.”

In the case of Golden Bella Holdings Ltd[7], ITAT held that the mere fact that the investment was funded using a portion of an interest free shareholder loan shall not deprive the Cyprus entity from enjoying the concessional rate of 10% withholding taxes as per Article 11 of India-Cyprus treaty. It was held that the Cyprus entity is not a conduit to be subject to tax at 42% but a beneficial owner of interest income.

Key international judicial precedents in the context of BO are mentioned below:

The Canadian Court in the case of Prévost Car Inc. v The Queen[8]concluded that beneficial owner is the person who receives dividends for his own use and assumes the risk and control of the dividend and is not accountable to anyone for how he deals with it. However, where the person receiving the dividend is obligated to pass on such dividends to a third party, such a person would not be considered as a beneficial owner of the dividends.

This decision reaffirms the principle that while examining BO rule, the corporate veil of the entity earning income should be respected unless the corporation is a conduit and has no discretion to deal on its own with the property put through it as a conduit or is acting as an agent, trustee or nominee of its shareholders.

A similar view is taken by the Canadian Court in the case of Velcro Canada v The

Queen[9].

The UK Court of Appeals in the case of Indofood International Finance Ltd. v JPMorgan Chase Bank NA, London Branch[10] held that an interposed entity between the beneficiary and the ultimate payer with a back-to-back debt obligation would not qualify as the beneficial owner of such interest income. The UK Court of Appeals arrived at its conclusion on the application of the ‘substance over form’ approach.

The Federal Administrative Court of Switzerland[11]while determining the BO of dividend under DTAA between Switzerland and Denmark, held that the concept of BO as stated in double tax convention, has to be interpreted based on ‘substance over form’ approach. The beneficial owner is defined as a person who has broad discretion to decide how dividend shall be utilised. In the facts of the said case, the Federal Administrative Court observed that, although the taxpayer had a duty to compensate the counterparty of a total return swap for the appreciation of the underlying shares, including dividend payments distributed during the maturity of the derivative, the total return swap did not include any contractual obligation for the taxpayer to hedge its position with the acquisition of the underlying assets. The Court then observed that there was no factual obligation to transfer any dividend income to the counterparty, as the taxpayer was only obliged to pass on an amount equal to the dividend, irrespective of whether it had effectively received a dividend payment. Hence, the fact that the taxpayer, by hedging its exposure from the total return swaps, was able to use the dividends for other purposes played a crucial role in strengthening the BO. The Federal Administrative Court further clarified that the effective holding period of the shares has no impact on the BO.

However, it is pertinent to note that in respect of the above decision, on further

appeal by the Swiss Federal Tax Authority (SFTA), the Federal Supreme Court (FSC)[12] reversed the decision of the Federal Administrative Court and upheld the view of SFTA. The FSC observed that there also is an implicit BO requirement in treaties that do not explicitly mention BO. BO requires, as a first element, that at the time of receiving a dividend, the recipient of a dividend has an unconstrained right to use, enjoy and dispose of the dividend received. If the recipient has a (legal or factual) obligation to pass on the dividend received to a third party under a derivatives contract, BO is denied.

Furthermore, the beneficial owner must bear the economic risk of whether a dividend is distributed or not. Where such risk is passed on to a counter-party to a derivatives contract, BO is denied. The derivatives contracts entered into by the Danish banks were accurately matching their investment in the underlying, both in volume and timing. The derivatives were entered into when the underlying shares were acquired and were terminated when the shares were sold. At the time when the dividend was received by the Danish banks, they had an obligation to pass it on to third parties under the total return swap or futures contracts, so that both the risks and rewards of the investment in the Swiss shares were substantially with the third parties and not with the Danish banks, which made only a small profit from these transactions.

Factors for determining BO – The PURC Matrix

Based on the meanings and judicial decisions discussed above, the PURC (Possession, Use, Risk, Control) matrix is a widely regarded test of BO. The elements of the PURC matrix need to be cumulatively fulfilled in order to satisfy the BO condition.

A brief discussion on each element is tabulated below:

Possession

This refers to possession of income which is substantiated by factors like receipt of income, exercise of dominion over income and property and valid economic, commercial purpose for the transaction.

Further, the recipient should not be acting as a mere conduit, nominee or agent.

Legal ownership, ultimate control and holding period of shares are irrelevant factors for fulfilling this element

Use

The recipient must have full right to directly benefit from the income and must be free to decide the manner of using the income so earned i.e. there should not be any contractual/ legal obligation to pass the income so earned

An adverse factor denoting lack of use by the recipient is that the right to use and enjoy is constrained by interdependency between obtaining an income and an obligation to pass it on.

Risk

The recipient must bear the business risk of the income in order to satisfy this element of the matrix. The recipient must be the economic owner i.e. he must bear the consequences of loss as well as enjoy the fruits of income. Further, his liability towards creditors must not be affected by lack of receipt of the income.

Any contractual agreement to pass on the risk of bad debt, loss, exchange fluctuation is indicative of lack of risk of the recipient.

Control

The recipient must retain full control over the income. Even in absence of explicit contractual agreements, the Revenue Authorities have regarded common Board of Directors (between the recipient and the alleged beneficial owner) as a sufficient factor for determining that the recipient does not have control over the income.

However, merely because of a holding-subsidiary relationship, it should not be assumed that the subsidiary company does not retain control of the income.

Based on the above, it can be concluded that the evaluation of BO is a highly fact specific exercise and there is no one-size-fits-all approach for the evaluation.

Way forward – Is evaluating BO a Pandora’s box?

The evaluation of BO requires a careful study of the facts of the case and is an evolving matter in the courts of law. For instance, as discussed above, in some cases Revenue Authorities have held that merely having a common director leads to non-fulfilment of the ‘Control’ element; however, having common directors across group entities is a normal business practice and driven by commercial considerations – all of which are seldom considered by the Revenue Authorities.

Given the recent amendment on taxation of dividends in the hands of the investors, the BO test would be required to be fulfilled by foreign investors seeking to avail tax treaty benefits for such dividend income. Thus, litigation around the overall concept of BO may increase.

Also, the determination of BO will be a time-consuming activity, both for the Assessing Officer (in terms of understanding complex multinational group structures and applying the concept of BO) and the taxpayer (in terms of collating documentation). Similar to approach adopted under GAAR, the Indian Revenue Authorities should release a guidance on the BO to provide certainty on the matter.

Chartered Accountants are also required to issue certificate in Form 15CB certifying applicability of beneficial rate under DTAA which will include satisfying the BO test. CAs must ensure that there is adequate documentation on record to substantiate that the foreign investor is indeed fulfilling the BO test. Where BO has not been evaluated, it would be a worthwhile exercise to undertake the same before certifying applicability of beneficial rate under DTAA.

One can equate BO test as being akin to Pandora’s box – once it is opened i.e. BO is evaluated, it can bring upon unexpected troubles and hurdles to the taxpayer in the form of never-ending litigation. That being said, just like Pandora’s box, there does remain ‘hope’ – that the tax authorities are able to provide clarity around the issue to promote Ease of doing business in India instead of resorting to frivolous litigation!

In order to implement the Base Erosion and Profit Shifting (BEPS) Action Plans, the Organisation for Economic Co-operation and Development (OECD) released the text of the Multilateral Instrument (MLI) in November 2016 to implement treaty related BEPS measures into more than 3000 existing treaties in a synchronised and swift manner.

India became a signatory to the MLI at the Paris conference on 7 June 2017 and deposited its ratified instrument with the OECD Depository on 25 June 2019, thus seeking to modify its Double Taxation Avoidance Agreements (DTAAs). The DTAA modified by the MLI is referred to as a Covered Tax Agreement (CTA).

It is pertinent to note that the MLI is not akin to a Protocol i.e. it does not directly amend the text of the CTA but has to be read alongside the existing CTAs. Further, the MLI does not modify all the CTAs in the same manner. Each MLI signatory is free to choose to apply provisions of the MLI (except minimum standards) and the list of each signatory’s position on each provision should be submitted with the OECD at the time of depositing the ratified instrument.

Need for synthesised text

As countries can choose the MLI provisions which they want to incorporate in their CTAs, one will need to consider the following documents while evaluating the impact of MLI on a specific provision of the CTA:

1. The text of the CTA along with the Protocol (if any);

2. The text of the provision(s) of the MLI; and

3. The list of notifications and reservations submitted by both the parties to the OECD.

For instance, to evaluate the impact of Article 8 of the MLI (dividends) on the existing India- Slovak Republic CTA, one will be broadly required to follow the below steps:

Check whether India and Slovak Republic are signatories to the MLI

Check whether India has notified Slovak Republic in its list of covered CTAs

Check whether Slovak Republic has included India in its list of covered CTAs

Refer India’s ratified instrument to check whether it has opted to apply Article 8 of MLI for its CTA with Slovak Republic

Refer Slovak Republic’s ratified instrument to check whether it has opted to apply Article 8 of MLI for its CTA with India

Where the answer to all the above steps is in the affirmative, Article 10 of the India- Slovak Republic CTA will stand modified by Article 8 of the MLI.

Needless to say, to undertake the above exercise for each Article of each CTA is highly cumbersome and tedious and increases the risk of errors while determining taxability and rates. This gave birth to the need of a comprehensive document providing the existing CTA along with the modifications made by the MLI – a Synthesised Text.

Meaning of Synthesised Text

The dictionary meaning of the word synthesis is “the combination of components or elements to form a connected whole”. This is what the synthesised text of a CTA does – it combines articles of the CTA and the modification proposed by the articles of the MLI.

In the synthesised text, the provisions of the MLI that are applicable with respect to the provisions of the CTA are included within “boxes” throughout the text of the CTA in the context of the relevant provisions of the CTA.

On 14 November 2018, the OECD released a “Guidance for development of synthesised texts” to provide suggestions to MLI signatories for the development of synthesised texts in order to facilitate the interpretation and application of modification proposed by articles of the MLI to the respective CTAs.

To ensure clarity and ease of reference on application of MLI, it is imperative that the synthesised texts of each CTA are as consistent as possible. Thus, the OECD Guidance also suggests sample language that may be included while preparation of synthesised texts.

Key features of synthesised texts as per the OECD Guidance

1. Not a legal document

The purpose of synthesised texts is primarily intended to facilitate the understanding of the MLI. For legal purposes, the provisions of the MLI must be read alongside Covered Tax Agreements as they remain the only legal instruments to be applied.

The synthesised text does not constitute a source of law and cannot be construed as a legal document admissible in a court of law.

2. Form of synthesised text

To be prepared in the form of a single document or webpage, the synthesised text would reproduce (a) the text of CTA (including the texts of any amending protocols or similar instruments), and (b) the provisions of the MLI that will modify that CTA in the light of the interaction of the MLI positions both the parties have taken.

Synthesised texts would also include explanatory information, including information on the entry into effect of the relevant provisions of the MLI.

Synthesised texts would thereby make it much simpler to understand the effects of the MLI and the way it modifies each CTA.

3. Prepared qua each CTA

Before developing synthesised texts, each MLI signatory is encouraged to integrate the effects of any existing amending instruments or protocols into the CTA.

4. No legal obligations on countries to develop synthesised texts

MLI signatories are not legally obligated to prepare synthesised texts for each of their CTAs and such synthesised texts are not a pre-requisite for application of MLI to the CTA.

5. No legal obligation on countries to consult each other while preparing synthesised texts

While there is no pre-requisite for countries to consult each other for preparing synthesised texts, the OECD encourages countries to do so. This is a good administrative practice and will help to ensure a consistent interpretation of the application of the MLI’s provisions to each Covered Tax Agreement.

When a synthesised text is prepared in consultation with the CTA partner, the following text is added to the synthesised text of the CTA:

“This document was prepared jointly by the Competent Authorities of Country A and Country B and represents their shared understanding of the modifications made to the Agreement by the MLI.”

This does not dilute the fact that the synthesised text is for understanding purpose only and not the legal document. Thus, the legal value of a unilateral or a bilaterally prepared synthesised text remains the same i.e. Nil.

Issues in unilateral synthesised texts of India-Japan CTA

On 23 August 2019, the Japan Ministry of Finance released the unilateral synthesised text of the India- Japan CTA and subsequently, on 4 September 2019, India’s Cen Japan CTA.tral Board of Direct Taxes (CBDT) released their unilateral synthesised text of the India-

Given that India and Japan have prepared separate synthesised texts without consultation with each other, it has resulted in inconsistent interpretation of the compatibility clauses of two provisions by India and Japan. The analysis of the discrepancies is provided below:

1. Discrepancy in Article 12(1) of the MLI

12(1) – Dependent Agent PE [seeking to modify Article 5(7)(a) of the India- Japan CTA]

India has not deleted the text of Article 5(7)(a) of the India – Japan CTA and has stated that Article 12(1) applies to Article 5(7)(a).

Japan has deleted the text of Article 5(7)(a) of the India – Japan CTA and has stated that Article 12(1) replaces Article 5(7)(a).

A combined reading of the compatibility clause of Article 12(1) and Article 12(5) states that the MLI provision shall apply “in place of” the existing clause in the CTA i.e. Article 12(1) shall replace the Dependent Agent PE provision in the CTA

Japan’s interpretation on applicability of Article 12(1) seems to be the correct interpretation of the compatibility clause of Article 12(1) of the MLI provisions.

2. Discrepancy in Article 17(1) of the MLI

17(1) – Corresponding adjustment [seeking to modify Article 9(2) of the India- Japan CTA]

India has deleted the text of Article 9(2) of the India – Japan CTA and has stated that Article 17(1) replaces Article 9(2).

Japan has not deleted the text of Article 9(2) of the India – Japan CTA and has stated that Article 17(1) applies to Article 9(2).

Japan has notified Article 9(2) of the India- Japan CTA to be modified by the MLI whereas India has not notified Article 9(2) of the India- Japan CTA. In such a scenario, as per Article 17(4) of the MLI, Article 17(1) shall apply and supersede the existing Article 9(2) of the India- Japan CTA only to the extent such clause is incompatible with the MLI provision.

In light of the above, India’s interpretation that Article 17(1) shall replace Article 9(2) may not be the correct interpretation. Further, Japan’s interpretation that Article 17(1) applies to Article 9(2) also seems to be incomplete since the synthesised text does not mention that the changes proposed by MLI shall be applicable only to the extent of incompatibility.

One may note that the above discrepancies do not have any legal ramifications in absence of the synthesised text being a binding legal document.

Way forward

With effect from 1 April 2020, the impact of MLI is to be considered in some of India’s key tax treaties – with Singapore, United Kingdom, Japan, Netherlands, France etc. and the list will only increase in the years to come. While the synthesised text captures articles of the CTA and the modification proposed by the articles of the MLI in a single document, one cannot rely on it in the Courts since it is not a legally binding document.

Use of synthesised text can be regarded as akin to looking up a legal query on the Google search engine- while it is good as a reference point, one cannot merely rely on the results produced by the search engine to give a legal opinion.

Similarly, while evaluating the impact of MLI, the synthesised text can be a good starting point but should always be backed up by comprehensive reading of the text of the CTA, the protocol(s) to the CTA, the text of the MLI and the positions adopted by both the Contracting Jurisdictions to arrive at the accurate answer.