Managing finances is one of the most important parts of running a successful business. However, many business owners often confuse bookkeeping and accounting. While both are related to financial management, they serve different functions.

Understanding the difference between bookkeeping and accounting can help businesses manage finances more efficiently and make better financial decisions.

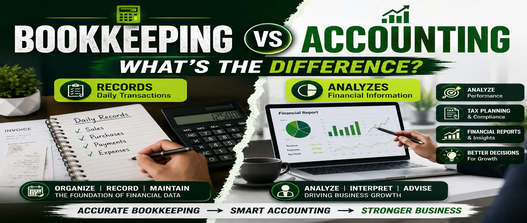

What is Bookkeeping?

Bookkeeping is the process of recording, classifying, and organizing daily financial transactions.

It includes:

- Recording sales and purchases

- Tracking expenses and income

- Managing invoices and receipts

- Maintaining bank records

- Recording payments and transactions

The main goal of bookkeeping is to maintain accurate financial records for the business.

In simple words, bookkeeping focuses on collecting and organizing financial data.

What is Accounting?

Accounting is the process of analyzing, interpreting, and reporting financial information collected through bookkeeping.

An accountant helps businesses:

- Prepare financial reports

- Calculate taxes

- Analyze profits and losses

- Ensure legal compliance

- Plan budgets and financial strategies

Accounting helps business owners understand the financial health of their business.

Main Difference Between Bookkeeping and Accounting

The biggest difference is that bookkeeping focuses on recording financial transactions, while accounting focuses on analyzing financial data.

A bookkeeper maintains records.

An accountant uses those records to provide financial insights and business advice.

For example:

- A bookkeeper records your monthly business expenses

- An accountant analyzes those expenses to help improve profitability and reduce taxes

Both functions work together and are equally important.

Why Bookkeeping is Important

Proper bookkeeping helps businesses:

- Stay financially organized

- Track income and expenses accurately

- Avoid missing transactions

- Prepare for tax filing

- Reduce financial confusion

Without bookkeeping, businesses may struggle with inaccurate records and compliance issues.

Why Accounting is Important

Accounting helps businesses make smarter financial decisions.

It helps with:

- Tax planning

- Business growth strategies

- Profit analysis

- Budgeting and forecasting

- Compliance management

Good accounting allows business owners to understand where money is coming from and where it is being spent.

Can Small Businesses Manage Without Them?

Many small businesses try to manage finances without proper bookkeeping or accounting. This often leads to:

- Cash flow problems

- Tax filing errors

- Missed deductions

- Financial confusion

- Compliance penalties

Even small businesses and freelancers benefit greatly from maintaining proper financial records.

Digital Accounting in 2026

Today, businesses are using software like:

- Tally

- Zoho Books

- QuickBooks

These tools simplify bookkeeping and improve financial accuracy.

However, software alone is not enough. Professional accounting expertise is still important for tax planning, compliance, and financial strategy.

Which One Does Your Business Need?

The answer is simple — most businesses need both.

- Bookkeeping keeps financial data organized

- Accounting helps businesses understand and use that data effectively

As a business grows, proper bookkeeping and accounting become even more important for maintaining financial stability and compliance.

Final Thoughts

Bookkeeping and accounting are both essential parts of financial management, but they serve different purposes.

Bookkeeping records daily financial transactions, while accounting analyzes financial information to support better business decisions.

A simple way to understand the difference is:

Bookkeeping records the financial story of a business, while accounting explains what that story means.

Businesses that maintain proper bookkeeping and accounting systems are usually more organized, financially stable, and better prepared for future growth.